The Spousal IRA Rollover Mistake That Triggered a $100,000 Penalty.

Lucy inherited more than $2.5 million in IRA assets from her late husband, Bill. As a surviving spouse, she had several choices for handling the account.

Lucy inherited more than $2.5 million in IRA assets from her late husband, Bill. As a surviving spouse, she had several choices for handling the account.

You’ve worked and saved all your life and have built a large retirement nest-egg. And if inflation hasn’t been bad enough—a million dollars isn’t what it used to be— you now face other issues – tax traps!

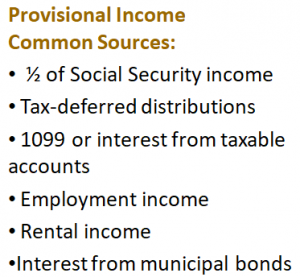

Retirement planning isn’t just about how much you’ve saved—it’s about not getting clobbered with excess taxes later. Managing RMDs is key!

Think a million dollars guarantees an easy retirement? See what a $1M portfolio really buys today, how far it goes in real life, and why your plan matters more than the number.

If you’ve built a large retirement nest egg, you’ve also built a large tax problem.

If you’re within 5-10 years of retirement and have built a portfolio north of $1 million, congratulations—you’ve done the hard part. Now, it’s about avoiding retirement mistakes.

Why are QLACs getting a attention now? Two reasons: (1) SECURE Act 2.0, and (2) rising interest rates.

Believe it or not, you’ll have a number of options available to you – and it pays to do your homework before making decisions that could be irrevocable – and costly.

But Congress Could Provide the Wild Card. Roth accounts can be attractive, especially when viewed through the lens of our national debt and the possibility (probability?) of higher taxes in the future to fund that debt.