IFG Viewpoint & Outlook

No Tax on Social Security Benefits?

We all love free money; and no taxes on Social Security sounds good! Hey, Social Security benefits weren’t taxed for many years!

We all love free money; and no taxes on Social Security sounds good! Hey, Social Security benefits weren’t taxed for many years!

Social Security decision-making isn’t as easy as it was for our parents and grandparents. When they became eligible, they simply went downtown (remember those places?) and simply filed.

Not so easy today. Social Security decision-making has become more complex and, unfortunately, because of that, there are few ‘simple’ answers.

Social Security claiming decisions aren’t as simple as they may appear. The decisions you make for yourself can impact your spouse, your future taxes, and even the bite Medicare premiums take from your Social Security benefits.

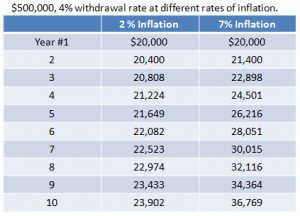

Many people believe they should take Social Security early in order to keep from drawing down IRA assets, believing that the longer they can grow the IRA tax-deferred, the better off they’ll be.

Are they wrong? Maybe. Maybe not. Different people are in different circumstances.

There have been some changes to Social Security this year.

Too many seniors still take the Social Security claiming decision too lightly – it’s a mistake that can cost them tens, if not hundreds, of thousands of dollars of retirement income during their lifetimes. And, often, the decision is made based on false bias or assumptions rather than a solid planning strategy.

Mistakes can be costly – and may be permanent!

For some people, planning for retirement can feel like trying to eat an elephant; but, it doesn’t have to be that way. Before making big decisions, it’s always important to get the ducks lined-up first.

Have you tried to call Social Security lately? If so, this won’t come as much of a surprise – customer service is all but non-existent.

The annual Social Security trustees’ report is to advise Congress on the financial condition of the Social Security system over the next 75 years. If they project that 100% of benefits will be paid, it’s said to be in balance and no action will be needed. If they project a shortfall, they call on Congress to fix the problem by either raising taxes, cutting benefits, or some combination of the two.