Is $2 Million Enough to Retire Comfortably in California?

A $2 million portfolio may be enough to retire comfortably in California, but the answer depends on spending, taxes, Social Security, Medicare, housing, and how withdrawals are managed.

A $2 million portfolio may be enough to retire comfortably in California, but the answer depends on spending, taxes, Social Security, Medicare, housing, and how withdrawals are managed.

Tax planning should be an integral part of your financial plan

It’s a typical question posed to AI. The simple answer is it cannot, by itself, answer the big one people are asking more often: Can AI Tell Me When I Can Retire?

Think a million dollars guarantees an easy retirement? See what a $1M portfolio really buys today, how far it goes in real life, and why your plan matters more than the number.

Think of treating inflation like a tough par-4 in a crosswind. You can’t control the wind— but you can control your stance, balance, club and shot selection.

If you’re within 5-10 years of retirement and have built a portfolio north of $1 million, congratulations—you’ve done the hard part. Now, it’s about avoiding retirement mistakes.

The Big Picture:

For years, baby boomers drove the housing market, and much of the economy, as they moved into their first homes, began raising families, and moved-up to larger homes finally ending-up in the “McMansions” we’re all familiar with today. The boomers are now older—they’re no longer moving up. In fact, they’re just beginning to “decumulate” and downsize.

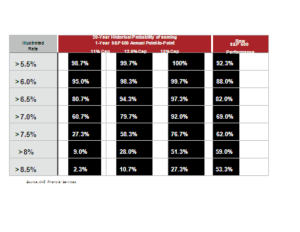

If you are one of those asking the ‘will my money last’ question, there’s a way you can find out just what your probabilities are!

When it comes to building a solid financial future, finding the right investment vehicle can be a daunting task. Comparisons are often made between an IUL (Indexed Universal Life Insurance) and a Roth IRA (Individual Retirement Account) as a choice between getting life insurance or investing in the stock market. While an IUL can give the appearance of doing both; however that’s not really the case – and, often, this can lead to unrealistic expectations.

Making your retirement nest-egg last through retirement isn’t easy. Company pension plans have all but disappeared, which means it’s now up to you to be your own actuary. Unfortunately, it’s not something many are equipped to do.