Can AI Tell Me When I Can Retire?

It’s a typical question posed to AI. The simple answer is it cannot, by itself, answer the big one people are asking more often: Can AI Tell Me When I Can Retire?

It’s a typical question posed to AI. The simple answer is it cannot, by itself, answer the big one people are asking more often: Can AI Tell Me When I Can Retire?

Think a million dollars guarantees an easy retirement? See what a $1M portfolio really buys today, how far it goes in real life, and why your plan matters more than the number.

Think of treating inflation like a tough par-4 in a crosswind. You can’t control the wind— but you can control your stance, balance, club and shot selection.

Short answer up front: if you’re healthy and can afford to wait, 70 usually wins on lifetime dollars; if cash flow is tight or your health isn’t great, earlier can make sense.

If you’ve built a large retirement nest egg, you’ve also built a large tax problem.

If you’re within 5-10 years of retirement and have built a portfolio north of $1 million, congratulations—you’ve done the hard part. Now, it’s about avoiding retirement mistakes.

The Big Picture:

For years, baby boomers drove the housing market, and much of the economy, as they moved into their first homes, began raising families, and moved-up to larger homes finally ending-up in the “McMansions” we’re all familiar with today. The boomers are now older—they’re no longer moving up. In fact, they’re just beginning to “decumulate” and downsize.

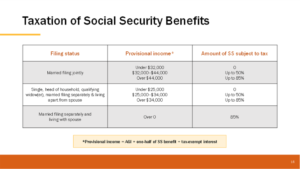

We all love free money; and no taxes on Social Security sounds good! Hey, Social Security benefits weren’t taxed for many years!

If you are one of those asking the ‘will my money last’ question, there’s a way you can find out just what your probabilities are!