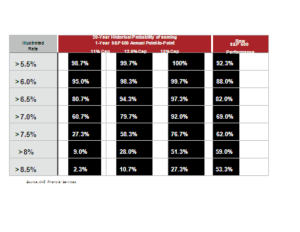

Annuities

How Can You Make Your Retirement Money Last?

Making your retirement nest-egg last through retirement isn’t easy. Company pension plans have all but disappeared, which means it’s now up to you to be your own actuary. Unfortunately, it’s not something many are equipped to do.