Planning

Remember 1966? How About 1967?

Retirement decisions can be momentous. Which year you would have remembered would depend on if you retired back then… and which year!

Retirement decisions can be momentous. Which year you would have remembered would depend on if you retired back then… and which year!

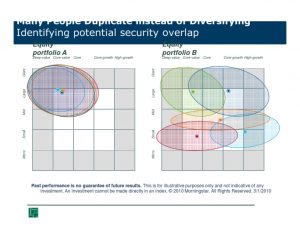

No investment strategy is without some kind of risk; but, I think this comes close. Take a look:

The annual Social Security trustees’ report is to advise Congress on the financial condition of the Social Security system over the next 75 years. If they project that 100% of benefits will be paid, it’s said to be in balance and no action will be needed. If they project a shortfall, they call on Congress to fix the problem by either raising taxes, cutting benefits, or some combination of the two.

Congress labeled it the SECURE Act, because it’s a better sell to the public. But, what Uncle Sam really wanted to do was make their spending programs more secure – hence, securing reelection.